In line with the Monetary Policy Committee’s (MPC) task to evaluate, determine, and provide transparency on the monetary policy actions of the Central Bank of Aruba (CBA), the CBA communicates the following. During its meeting of February 26, 2024, the MPC decided to maintain the reserve requirement rate unchanged at 22.0 percent as of March 1, 2024. Accordingly, commercial banks must hold a minimum balance at the CBA equal to 22.0 percent of their clients’ liquid deposits. The decision to maintain the reserve requirement rate unchanged was based primarily on the official reserves being relatively close to the lower bound of the ARA metric, even though both the official and international reserves are still adequate and are foreseen to remain so during 2024. Furthermore, excess liquidity held at the commercial banks has been on an upward trend in recent months. Finally, maintaining the reserve requirement rate at its current level is considered prudent, given the continued uptick in loans and its potential effect on the international reserves. The CBA continues to monitor reserves and the excess liquidity developments, and stands ready to adjust the reserve requirement rate, if deemed necessary.

The MPC considered the following information and analysis during its deliberations.

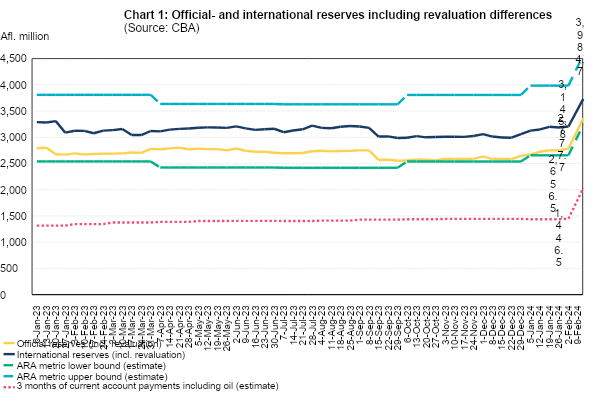

International and official reserves

The international reserves, comprising the official reserves of the CBA and foreign reserves held by the commercial banks, increased by Afl. 83.8 million as of February 9, 2024, compared to December 29, 2023 (Chart 1). Official reserves expanded by Afl. 132.0 million, while the foreign reserves at the commercial banks dropped by Afl. 48.2 million. Consequently, as of February 9, 2024, official and international reserves amounted to Afl. 2,777.7 million and Afl. 3,145.8 million, respectively.

Conserving reserve adequacy is critical in maintaining the fixed exchange rate between the Aruban florin and the US dollar. In this regard, international reserves stayed comfortably above the minimum required three months of current account payments as of February 9, 2024. Current account payments consist, among others, of import payments, interest payments made to investors, and foreign transfers, such as remittances by foreign workers. Official reserves also stayed within an adequate range when benchmarked against the International Monetary Fund’s (IMF) Assessing Reserve Adequacy (ARA) metric (Table 1).

| Table 1: Reserve benchmarks monitored over the past 12 months | ||||||||||||

| 2023 | 2024 | |||||||||||

| Feb | Mar | Apr | May | Jun | Jul | Aug | Sep | Oct | Nov | Dec | Jan | |

| Estimated current account coverage ratio1 | 7.0 | 6.8 | 6.9 | 6.8 | 6.7 | 6.9 | 6.8 | 6.2 | 6.2 | 6.3 | 6.3 | 6.5 |

| Estimated IMF ARA Metric2 | 105.3 | 109.6 | 114.9 | 113.5 | 111.8 | 113.4 | 113.7 | 105.9 | 105.5 | 102.2 | 103.4 | 106.8 |

| ¹ The number of months of current account payments covered by the international reserves.² The ratio between the level of official reserves and the minimum adequate level (following the IMF), in percent. | ||||||||||||

Inflation

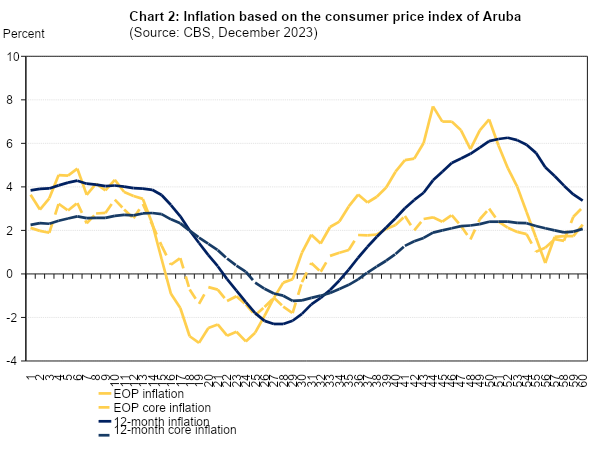

The end-of-period inflation (EOP) stood at 2.3 percent in December 2023 (Chart 2). The main contributors to the EOP inflation in December 2023 were ‘communication’ (+1.6 percentage points contribution), ‘miscellaneous goods and services’ (+0.4 percentage point contribution), and ‘housing’ (+0.4 percentage point contribution). On the other hand, the transport component mitigated (-1.0 percentage point contribution) the EOP inflation in December 2023.

As of December 2023, the 12-month average inflation fell to 3.1 percent, down from 3.7 percent in November 2023. The inflationary pressures were mostly due to the hikes in water and electricity tariffs as of August 2022 and higher prices of food and non-alcoholic beverages. Furthermore, Aruba imported much of the rising prices from its trading partners, particularly the United States and Europe.

Meanwhile, in December 2023, EOP core inflation (which excludes energy and food) was 3.1 percent (2.6 percent in November 2023). On a twelve-month average basis, core inflation amounted to 2.1 percent (1.9 percent in November 2023).

Excess liquidity of the commercial banks

Excess liquidity (including undisbursed loan funds and other commitments) of the commercial banks stood at Afl. 519.4 million as of December 2023, i.e., an Afl. 78.7 million increase compared to November 2023 (Chart 3). When compared to end-December 2022, excess liquidity reflected a contraction of Afl. 300.4 million. This drop was mainly due to local refinancing of foreign loans and government bond purchases by institutional investors.

: More transparency needed in tourist tax plan")